When Can I Retire?

Let’s take the 25% yearly saving rate from the example above. In order to accumulate one year of expenses (i.e. 75% of income, as stated above), you would need to save for a total of 3 years (i.e. 25% x 3 = 75%). Thus, in order to save 25 times your yearly expenses, as the 4% rule recommends, you would need to save for 25 times longer, aka 75 years (i.e. 3 years x 25 = 75 years)! But aren’t we forgetting something here? You wouldn’t just be saving this money, you would be investing it in order to take advantage of compound growth! Let’s run some numbers.

Since the ultimate goal is to accumulate 25 times yearly expenses and in this example 75% of income is equal to yearly expenses, we can re-compute the goal amount as, 75% of income times 25, which equals 1875% of income (i.e. 75% x 25 = 1875%).

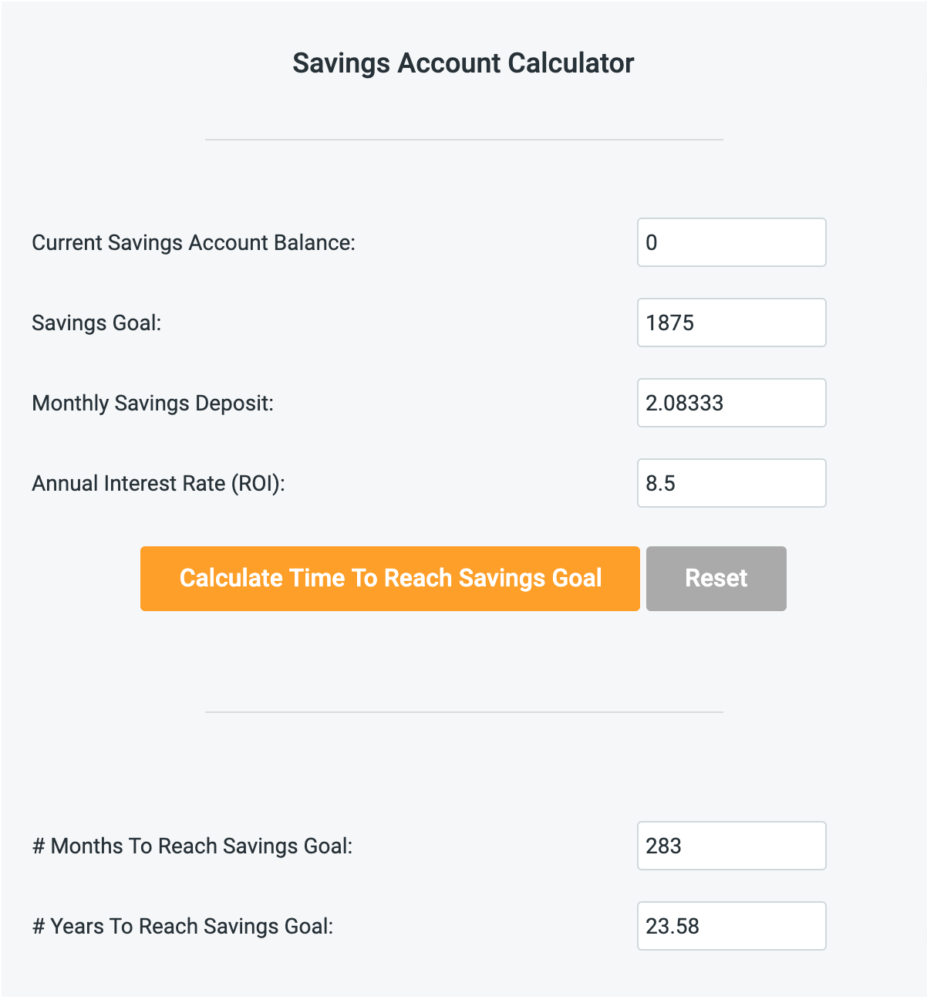

With that value, we now have all of the information we need to calculate our timeframe! It would be tedious to do by hand so we’ll take a shortcut by using a Savings Goal Calculator. We can enter our numbers as follows:

We assume that you are starting from $0, so Current Savings Account Balance is set to 0. For Savings Goal we use 1875, which we calculated above. For Monthly Savings Deposit we take our 25% yearly saving rate and divide it by 12 to get 2.08333 (i.e. 25% / 12 = 2.08333). Finally, for Annual Interest Rate we will use the historical stock market rate of return of approximately 8.5%. After entering the values into the calculator the result we get is 23.58 years (aka 283 months). So this means, anyone who saves and invests 25% of their income will have enough money to retire in exactly 23.58 years!

All of the calculations we have done are based solely on saving rate. The amount of income is never even considered. In our example, we demonstrated that anyone who manages to consistently save 25% of their income will accumulate enough to retire (i.e. 25 x yearly expenses) in about 23 and a half years, but why stop there? We can do this same set of calculations for any saving rate.

Tools To Get You Started

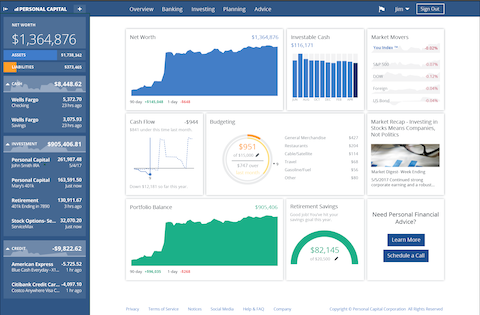

Get a head start on your journey toward achieving financial independence by analyzing and tracking your income, expenses, investment performance, and overall net worth with the free online wealth management tool Personal Capital.

We use Personal Capital regularly to analyze our investment fees, track our investments, and project our net worth. We also periodically review our progress toward retirement with their retirement planning calculator.

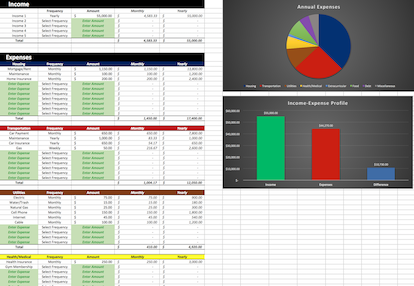

If you’d rather do things on your own, become a subscriber today and you’ll receive our Free Financial Planning Dashboard. This tool allows you to enter your income and expenses to create a detailed budget. You can use it to track your spending habits over time or just to get an idea of where your money is going each month. Take a look at the automatically generated charts and you may discover you have a little more cash to invest than you thought.

If you’re interested in detailed instructions on how to budget, save, pay off debt, and invest, check out The 6 Phases of Building Wealth. This book provides step-by-step instructions for working through each “Phase” in the process of achieving Financial Freedom. If you're just starting out, the information in this book will provide you with an invaluable resource. You can pick up the digital version for only $2.99 on Amazon.