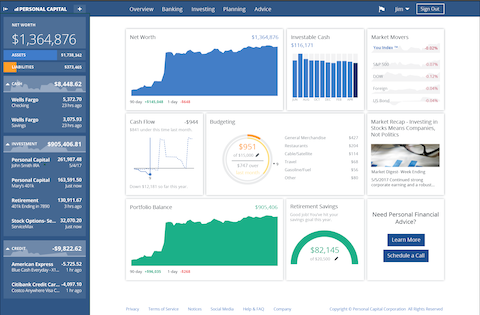

Scott and Charles, both 20 years old, have recently been hired for their first job. Scott is a big fan of GoGreenDollar and so on his very first day of work, he decides that each month he will contribute $500 of his paycheck to an investment account in preparation for retirement. Charles, on the other hand, is not interested in saving. He decides he’d rather spend all his income on expensive activities and items.

After 10 years Scott and Charles’ savings look vastly different.

Charles hasn’t saved any money for retirement. Now 30 years old, he realizes he’ll need to save something if he ever wants to stop working. He commits to reducing his spending and begins depositing $500 per month into his investment account.

After 10 years of investing, Scott has amassed a sizable nest egg. In total, he invested $60,000 of his own money (i.e. $500 x 12 months x 10 years) and averaged an 8.5% annual return. This has allowed Scott to save $94,223! Scott’s expenses have recently increased, however. Consequently, he has decided to stop making contributions to his investment account.

30 more years pass. Scott and Charles are now both 60 years old and preparing for retirement.

Charles has been investing $500 a month for the last 30 years and it has paid off big time. In total, he contributed $180,000 of his own money (i.e. $500 x 12 months x 30 years) and averaged an 8.5% annual return. Charles’ consistent contributions paired with the power of compound growth have propelled his savings from the $0 he had when he was 30, all the way to $830,322.

Scott, on the other hand, stopped contributing to his investment account at the age of 30 after he had accumulated $94,223. He hasn’t contributed a single dollar since then. He also hasn’t withdrawn any money. Over the last 30 years, Scott’s investments have continued to compound at an average rate of 8.5% per year. Having ignored his investment account for over 30 years, Scott is a bit worried that he hasn’t saved enough for retirement. He logs into his account and is shocked by what he sees. His balance has grown to a massive $1,206,361!!

| Year | Scott's Contributions | Scott's Savings | Charles' Contributions | Charles' Savings |

| 0 | - | $0 | - | $0 |

| 1 | $6,000 | $6,240 | $0 | $0 |

| 2 | $6,000 | $13,034 | $0 | $0 |

| 3 | $6,000 | $20,430 | $0 | $0 |

| 4 | $6,000 | $28,483 | $0 | $0 |

| 5 | $6,000 | $37,250 | $0 | $0 |

| 6 | $6,000 | $46,794 | $0 | $0 |

| 7 | $6,000 | $57,185 | $0 | $0 |

| 8 | $6,000 | $68,498 | $0 | $0 |

| 9 | $6,000 | $80,815 | $0 | $0 |

| 10 | $6,000 | $94,223 | $0 | $0 |

| 11 | $0 | $102,581 | $6,000 | $6,240 |

| 12 | $0 | $111,681 | $6,000 | $13,034 |

| 13 | $0 | $121,588 | $6,000 | $20,430 |

| 14 | $0 | $132,272 | $6,000 | $28,483 |

| 15 | $0 | $144,115 | $6,000 | $37,250 |

| 16 | $0 | $156,899 | $6,000 | $46,794 |

| 17 | $0 | $170,817 | $6,000 | $57,185 |

| 18 | $0 | $185,970 | $6,000 | $68,498 |

| 19 | $0 | $202,466 | $6,000 | $80,815 |

| 20 | $0 | $220,426 | $6,000 | $94,223 |

| 21 | $0 | $239,980 | $6,000 | $108,822 |

| 22 | $0 | $261,267 | $6,000 | $124,715 |

| 23 | $0 | $284,443 | $6,000 | $142,018 |

| 24 | $0 | $309,675 | $6,000 | $160,857 |

| 25 | $0 | $337,145 | $6,000 | $181,366 |

| 26 | $0 | $367,052 | $6,000 | $203,694 |

| 27 | $0 | $399,612 | $6,000 | $228,003 |

| 28 | $0 | $435,060 | $6,000 | $254,469 |

| 29 | $0 | $473,652 | $6,000 | $283,282 |

| 30 | $0 | $515, 668 | $6,000 | $314,651 |

| 31 | $0 | $561,411 | $6,000 | $348,803 |

| 32 | $0 | $611,212 | $6,000 | $385,984 |

| 33 | $0 | $665,430 | $6,000 | $426,463 |

| 34 | $0 | $724,458 | $6,000 | $470,533 |

| 35 | $0 | $788,722 | $6,000 | $518,512 |

| 36 | $0 | $858,686 | $6,000 | $570,748 |

| 37 | $0 | $934,857 | $6,000 | $627,617 |

| 38 | $0 | $1,017,784 | $6,000 | $689,531 |

| 39 | $0 | $1,108,068 | $6,000 | $756,936 |

| 40 | $0 | $1,206,361 | $6,000 | $830,322 |

| Final Total = | $60,000 | $1,206,361 | $180,000 | $830,322 |

Even though Charles contributed $120,000 more (i.e. $180,000 - $60,000 = $120,000) and continued making deposits over a much longer period, Scott still ended up with a significantly larger nest egg. $376,039 larger to be exact (i.e. $1,206,361 - $830,322 = $376,039). This difference demonstrates the powerful effect time has on the growth of an investment. Simply by starting early and letting his money grow over a longer duration of time, Scott was able to massively out-save Charles.

[…] Time Is Your Most Powerful Investing Tool […]