Tools To Get You Started

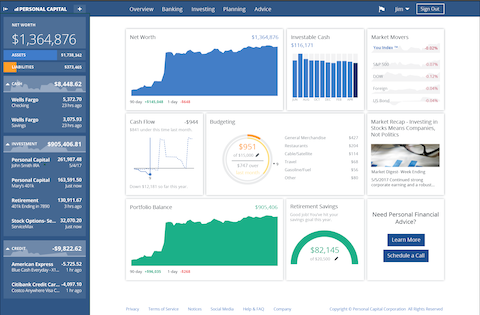

Get a head start on your journey toward achieving financial independence by analyzing and tracking your income, expenses, investment performance, and overall net worth with the free online wealth management tool Empower Personal Dashboard.

We use Empower Personal Dashboard regularly to analyze our investment fees, track our investments, and project our net worth. We also periodically review our progress toward retirement with their retirement planning calculator.

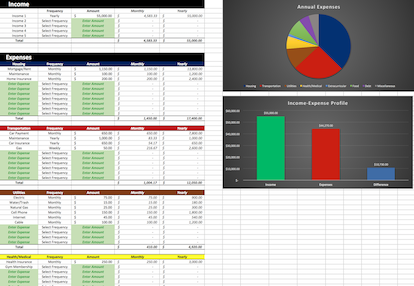

If you’d rather do things on your own, become a subscriber today and you’ll receive our Free Financial Planning Dashboard. This tool allows you to enter your income and expenses to create a detailed budget. You can use it to track your spending habits over time or just to get an idea of where your money is going each month. Take a look at the automatically generated charts and you may discover you have a little more cash to invest than you thought.

If you’re interested in detailed instructions on how to budget, save, pay off debt, and invest, check out The 6 Phases of Building Wealth. This book provides step-by-step instructions for working through each “Phase” in the process of achieving Financial Freedom. If you're just starting out, the information in this book will provide you with an invaluable resource. You can pick up the digital version for only $2.99 on Amazon.

[…] Go green Dollar […]

I’m sorry, but I have to disagree with you on this. While I accept the math, it is sort of like Dave Ramsey’s debt snowball – the math is wrong, but the human element makes it work better. Yes, if someone took the excess money and invested it, they will, in all probability, make more money. Yet you have to account for human faults (will they actually invest it, or will they blow it) and human weakness (ouch! the market dropped, let me pull my money out at the bottom of the market and retreat to 0.5% saving account). Getting… Read more »

I agree, there’s definitely always the human factor to consider. However, I think it would be a disservice to those who are laser-focused on financial independence for me to give advice that would result in a less beneficial financial outcome. Dave Ramsey definitely approaches things from a more realistic “human emotion” perspective, which is probably the reason he has such a broad audience. My goal, on the other hand, has always been to present what I feel is the BEST option. Not necessarily the easiest or most likely to be achieved/followed through on, but the option that will lead to… Read more »

Another option when pursuing financial independence via investing would be to skip home ownership altogether. There are so many other costs to home ownership besides the mortgage. Be a renter instead & invest as much as possible.

I’m definitely on the rent over buy train…

https://gogreendollar.com/renting-is-better-than-buying/

Interesting that this comes at a time when I have an article scheduled to publish in a few weeks. I go through the numbers in our scenario and have a poll that allows people to voice their opinion on which option they think is best. Given our exact situation, I calculated that if we do not pay extra towards our mortgage, in theory, we will have $500k more after 26-years in our after-tax investment account. That comes to $3.7m vs $4.1m over 26 years. I have a good mortgage rate at 3.625 and 26-years left on the mortgage. $500k is… Read more »

Yep, can’t deny the math. However, when human psychology is factored in, who knows how things would actually turn out for most people? I’d definitely like to check out your article!