Wake up, go to work, spend a few hours with family, go to bed, rinse and repeat.

Some form of this routine probably describes the typical day for most of us. Throughout our lives, we’re conditioned to believe that we should follow this monotonous series of actions for 30-40 years and, as a reward, we’ll get to spend our final few years enjoying ourselves in retirement. This tradition of working, basically until we die, has never sat well with me. Even as a kid, I couldn’t imagine myself working until old age. I felt that life should be about adventure and pursuing new experiences. I wanted to travel the world, taste all the foods, and see all the sights. How could I do this if I spent the vast majority of life either sitting in a cubicle at work or laying in bed sleeping? The answer was simple. I couldn’t. I needed to find a way out.

Thankfully, I have found the formula and it’s much simpler than you might imagine. It consists of three parts. The first is an easy calculation.

Part 1 Calculate Savings Rate

(Income – Expenses) / Income = Savings Rate

That’s it.

Once you know your savings rate, you can project exactly when you will be able to retire. Increase your savings rate and you’ll retire sooner, decrease it and you’ll need to work longer. Your savings rate determines both the amount of money you put away each year AND the amount of money you need to maintain your current lifestyle. With these numbers you can begin to plan your escape.

Here’s an example:

If Tom is able to save 50% of his income per year, this means that he uses the other 50% to cover all of his expenses. So by definition, he can maintain his lifestyle with 50% of his income. If we assume that Tom is saving all of this money in a jar under his bed, generating zero interest*, then after one year he will have the equivalent of 50% of his yearly income saved, or one year's worth of expenses. If Tom continues to do this, each year he will have saved an additional year's worth of expenses. After five years, he would have five years' worth of expenses saved (i.e. 50% of income x 5 years), after 10 years he’d have 10 years' worth, and so forth and so on. Using this math, after 30 years Tom (in his late 50’s or early 60’s) would have 30 years' worth of living expenses saved in his jar and would probably be able to safely retire. But wait, you say, “This is the exact situation we were trying to avoid.” You are absolutely right and that’s why we need to consider the second part of the formula, Investing.

*When inflation is considered, Tom would actually be generating a negative return. However we are ignoring inflation in favor of simplicity.

Part 2 Invest

Invest money and over time it grows. The more you invest, the more growth you will see. It can’t be that simple, right? Well…actually it is! Mostly. When you invest in broad market index funds (such as Vanguard’s VTSAX, VFINX, and VFIAX) for the long-term, you can expect an average return of about 7-10%. This is based on the last 100 years of stock market returns. There will be ups and downs along the way, but on average, over the long-term, 7-10% is a very reasonable expected rate of return. But how could this be? How could it be so simple? Well, the detailed answer to that question is complicated (and potentially very technical) but the simple answer is, the world grows and improves in efficiency over time leading to higher standards of living, larger populations (i.e. more consumers), and increased productivity from businesses. These things have been true for most of human existence and there is no reason to think they will change in the foreseeable future. All of this ultimately translates into ever-increasing stock prices. So, historically, money invested in the stock market over any long-term period (10-20+ years) would have seen amazing growth (don’t take my word for it, check the numbers yourself). How does this affect the formula? Let's go back to our example.

Assume, instead of storing the money under his bed, Tom invests the money in the stock market. Each month, he deposits half of his income into a total stock market index fund. Over time, he averages a 7% return rate. With compounding growth, his savings would look as follows:

| Years | % of yearly living expenses saved |

|---|---|

| 1 | 103% |

| 2 | 214% |

| 3 | 333% |

| 4 | 460% |

| 5 | 597% |

| 6 | 743% |

| 7 | 901% |

| 8 | 1,069% |

| 9 | 1,250% |

| 10 | 1,444% |

| 11 | 1,652% |

| 12 | 1,875% |

| 13 | 2,114% |

| 14 | 2,371% |

| 15 | 2,646% |

(You can use the calculators at Bankrate.com to run your own simulations.)

By investing the money and taking advantage of compound interest, after just 15 years, Tom has amassed a savings of over 25 times his yearly expenses (2,646% = 26.46 x yearly expenses). This is significantly better than the previous scenario in which he didn’t invest any of his funds. In fact, Tom now has enough to retire! How do I know he has enough? What makes the number 25 significant? The third, and final part of the formula explains.

Part 3 Determine Retirement Number

In order to be retired, you eventually have to stop working and live on what you have saved and invested. But how do you know when you’ve hit this number? Let me introduce you to the 4% rule. The 4% rule suggests that with a mix of stocks and bonds, you can withdraw 4% of your holdings each year (annually adjusted to keep pace with inflation) and the money should last at least 30 years.

The rule is based on a research paper called the “Trinity Study.” This study determined that a 4% withdrawal rate was extremely unlikely to exhaust an investment portfolio of stocks and bonds over a retirement period. So how do we use this knowledge to calculate our retirement number? Simply multiply your living expenses by 25.

This works out because 100% / 4% = 25. So your yearly living expense times 25 will give you 100% of the amount you need to save in order to withdraw 4% each year and meet your spending needs.

I realize there is a glaring issue with all this. The Trinity Study was completed with a 30-year period in mind. If I want to retire in my 30’s I may need the money to last 60 years or more!

Even though the Trinity Study was designed specifically to measure only 30-year periods, in the vast majority of cases, after 30 years of withdrawals, a hypothetical investor would be left with significantly more money than she had started with. In addition, the Trinity Study assumes you will never earn any money ever again from any other source (e.g. part-time work, side hustles, social security, etc.) and that you will never adjust your spending rate regardless of the current market conditions. For very early retirees, these assumptions are probably not very accurate. As a result, I think in general, assuming a 4% withdrawal rate (or 25 times expenses) is a pretty safe way to determine how much you need for a long-term retirement.

If you’re still a bit confused about the 4% rule, check out this article for a more thorough breakdown.

Let's do a final example to bring it all together.

We'll assume Tom’s salary is $60,000.

Each year he spends $30,000 and invests the rest (i.e. 50% savings rate).

Starting with $0, Tom begins on his path to retirement by depositing $2,500 per month ($30,000/12 months) into one of Vanguard's total US stock market index funds. Over 15 years (with an average 7% annual return), his investment will look as follows:

Years % of yearly living expenses saved Amount Saved

1 103% $30,984

2 214% $64,215

3 333% $99,855

4 460% $138,079

5 597% $179,074

6 743% $223,041

7 901% $270,196

8 1,069% $320,770

9 1,250% $375,010

10 1,444% $433,183

11 1,652% $495,574

12 1,875% $562,487

13 2,114% $634,253

14 2,371% $711,221

15 2,646% $793,769

Eventually, Tom accumulates almost $800,000 in his investment account. Since his retirement number is $750,000 (25 x $30,000), Tom has reached financial independence (FI) and he did it in 15 years, just as we predicted using only his savings rate!

But what if Tom had saved at a different rate?

The table below shows the approximate number of years Tom would have had to work at different savings rates (again, using a 7% average return).

Savings Rate Years Working Before Reaching FI

10% 42

20% 31

30% 24

40% 19

50% 15

60% 12

70% 9

80% 6

90% 3

100% 0

Final Thoughts

There are three important things you should take away from this article.

- The only number you need to determine when you will be able to achieve financial independence is your savings rate.

- If you desire to retire at some point in life, you MUST invest your money.

- Multiplying 25 x your yearly expenses will give you your retirement number.

Keep these things in mind next time you’re contemplating an exit strategy from corporate America and I’m confident you’ll be ahead of the curve.

Tools To Get You Started

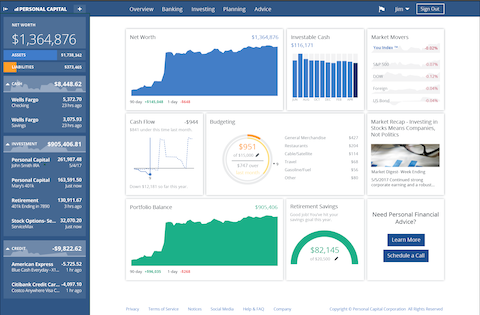

Get a head start on your journey toward achieving financial independence by analyzing and tracking your income, expenses, investment performance, and overall net worth with the free online wealth management tool Empower Personal Dashboard.

We use Empower Personal Dashboard regularly to analyze our investment fees, track our investments, and project our net worth. We also periodically review our progress toward retirement with their retirement planning calculator.

If you’d rather do things on your own, become a subscriber today and you’ll receive our Free Financial Planning Dashboard. This tool allows you to enter your income and expenses to create a detailed budget. You can use it to track your spending habits over time or just to get an idea of where your money is going each month. Take a look at the automatically generated charts and you may discover you have a little more cash to invest than you thought.

If you’re interested in detailed instructions on how to budget, save, pay off debt, and invest, check out The 6 Phases of Building Wealth. This book provides step-by-step instructions for working through each “Phase” in the process of achieving Financial Freedom. If you're just starting out, the information in this book will provide you with an invaluable resource. You can pick up the digital version for only $2.99 on Amazon.

Disclosure: Some of the links found on this website may be affiliate links. Affiliate links pay GGD a small commission when you click through and/or make a purchase. This is at zero additional cost to you.

Full Disclaimer/Disclosure

Related Posts

Surprisingly Simple Investment Strategy For Retiring Early

Surprisingly Simple Investment Strategy For Retiring EarlyThe other day, while browsing through YouTube videos, I came across one that featured Tony Robbins discussing investing. I watched the video and found it had some good, if not groundbreaking, suggestions. There was one…

The Basics: Compound Growth

The Basics: Compound GrowthIn the previous installment of “The Basics” series, we presented a step-by-step guide on how to set up your first investment account. Hopefully, that post will help some of the investment beginners out there conquer…

Investment Hierarchy: Top 7 Investments For Retiring Young

Investment Hierarchy: Top 7 Investments For Retiring YoungWhen you make the decision to become an early retiree, one of the first things you'll realize is that there are many, many different choices when it comes to investment accounts. 401(k), IRA, HSA, 457,…

Thank you for all your hard work!

No problem, thanks for reading!

Thanks for this. Implementing Now!

Nice! Let us know how it goes.

Wow, this is really explained well. I’m going to try some of these tips and see how it goes.

Great, I’m glad you’re able to take something away from this post. Keep me updated on how things turn out!

This is great information and very insightful…but what about those that are late to the party? What if Tom didn’t receive this information until later in life. Should Tom still work towards FI even though he is beyond the point of early retirement?

Great question! Even if you’re still working in your 50’s, 60’s, or even 70’s don’t feel bad about missing the party. It’s never too late to begin your journey towards financial independence. The beauty of the lessons discussed in this post is that they can be utilized by anyone, regardless of their age. Lets run through them…First, Investing is a MUST for anyone seeking to retire. If your money isn’t growing, then you’re actually losing money due to inflation. Second, calculating your retirement number will give you an idea of how much you might need in order to maintain your… Read more »

Easy to read, simple to understand and hopefully easy to implement – I hope you make people change.

Good luck!

Thanks! I hope this “formula” can help people as well!

Retirement at 30 years old, why not? Exactly I am now. I have worked 12 years and find that why I have to go to the office and face heavy traffic jam everyday. I am planning to open online business like sushi rice brands to have income and enjoy life more.

Thanks for sharing your formula. I am 32 years old now, so i think i can apply this into my case. So I can retire before 40s. Can I copy this post to my personal blog for more viewers?