Renting vs. Buying

Bill and Ted are both looking for a place to live. Bill wants to purchase a home while Ted would prefer to rent. They each have $57,500 in available cash to spend. Bill plans to use the money for his down payment and closing costs. Ted, on the other hand, has been reading about investing on GoGreenDollar and has decided that he’d like to invest his money in a total US stock market index fund. His landlord requires one month of rent as a deposit but he plans to invest the rest. Bill and Ted each plan to live in their home for the next 30 years.

Assumptions:

Home Value = $250,000

Available Cash = $57,500

Stock Investment Growth Rate = 9.25% per year

Property Value Growth Rate = 3.5% per year

Rent Growth Rate = 1.15% per year

Bill's Numbers:

Down Payment (20%) = $50,000

Closing Costs (3%) = $7,500

Mortgage Term = 30 years

Mortgage Rate (fixed) = 4.25%

Monthly Mortgage Payment = $984 per month

Monthly HOA Fees = $50 per month

Property Taxes (1%) = $2,500 = $208 per month

Maintenance/Renovation (1.5%) = $3,750 = $313 per month

Homeowner Insurance (0.5%) = $1,250 = $104 per month

Bill's Total Monthly Cost = $984 + $50 + $208 + $313 + $104 = $1,659 per month

Ted's Numbers:

Price-To-Rent Ratio = 17

Rent = $250,000 / 17 = $14,706 / 12 months = $1,226 per month

Deposit (1 months rent) = $1,226

Renters Insurances = $240 = $20 per month

Ted's Total Monthly Cost = $1,226 + $20 = $1,246 per month

Initial Monthly Spending Difference (Renting vs. Buying) = $1,659 - $1,246 = $413 per month

*The total difference in monthly expenses will be added to Ted’s investment account at the end of each year.

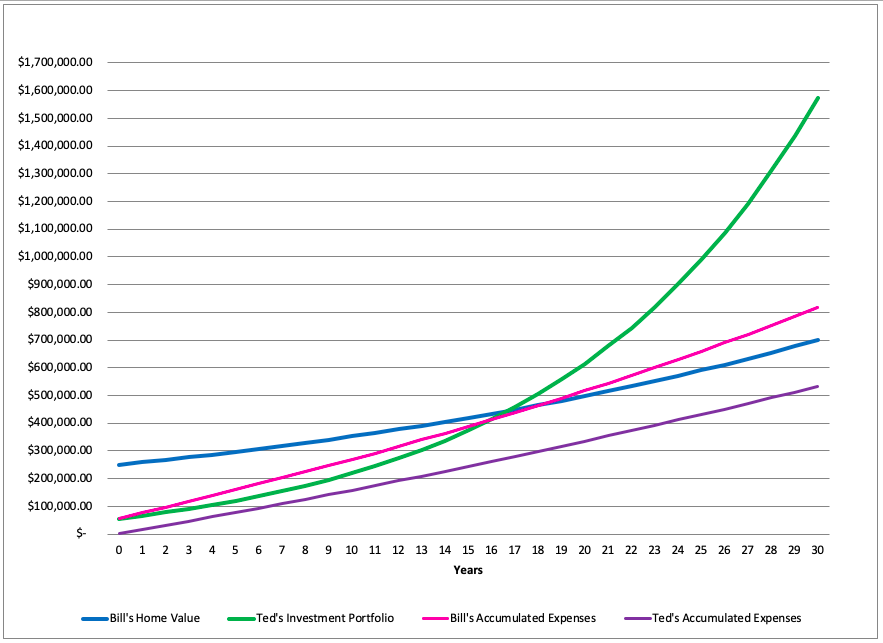

When we graph all of the data over a 30-year period we get the following:

All I can say is, WOW. As you can see from the chart, over a 30-year period, renting thoroughly defeats buying. It’s not really even close.

After 30 years, the value of Bill’s home has grown considerably, going from a starting value of $250,000 to an ending value of $701,698. That’s a huge increase of over 180%! When we compare this growth to that of Ted’s portfolio, however, it begins to seem pretty paltry.

By investing the remaining cash after paying his deposit (i.e. $57,500 - $1,226 = $56,274) in addition to the money he saved each year by being a renter, over a 30-year period, Ted was able to accumulate well over $1.5 million! That’s more than double the value of Bill’s home! I think it's safe to say that Ted has done pretty well for himself.

Note: Obviously, there are specific cities and neighborhoods around the nation where these numbers are drastically different. You may live in an area with hugely inflated rental rates and greatly undervalued home prices. If that happens to be your situation, it is possible you may find the difference between renting and buying to be less pronounced. Even in these cases, however, purchasing a home would still severely limit your freedom and significantly increase your risk.

Still Don't Buy It?

Even though every number used in the example was based on real data, I know some will still argue that the numbers are skewed. So let’s make it super simple. I’ll throw out all of the additional costs associated with owning a home and assume that Bill’s monthly payment is exactly the same as Ted’s. Now, the only difference between their circumstances is that Bill is buying his home while Ted is only renting his.

In order to buy his new home, Bill pays $57,500 for his down payment and closing costs.

Ted must deposit one month of rent, or $1,246, in order to move into his new place. He will invest the remainder (i.e. $56,254).

Assumptions:

Bill’s Home's Initial Value = $250,000

Ted’s Initial Investment Value = $56,254

Property Value Growth Rate = 3.5%

Stock Investment Growth Rate = 9.25%

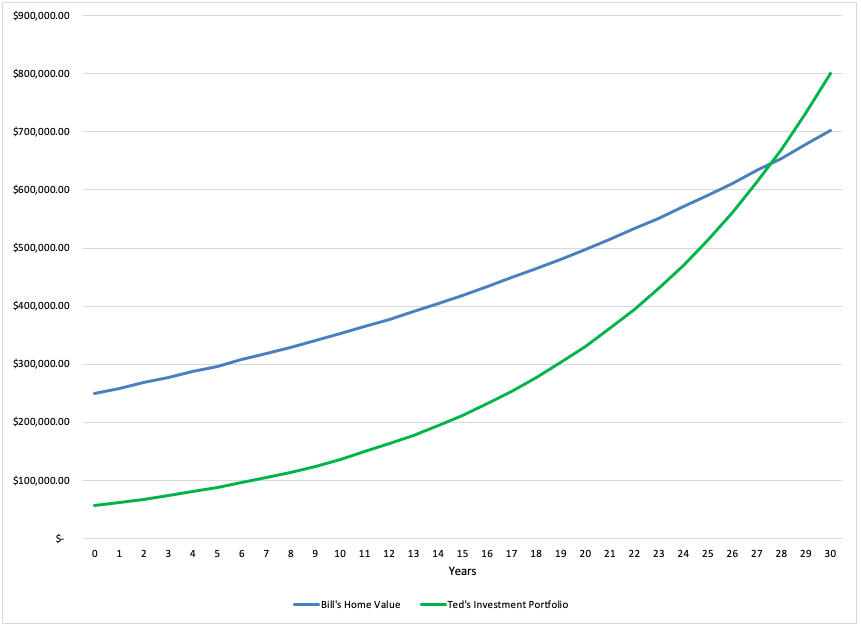

Just like in the previous example, after 30 years of steady growth, the value of Bill’s home has grown from $250,000 to $701,698. How has Ted fared?

Since the monthly expenses for Bill and Ted were exactly the same, Ted received no additional savings from renting. His initial investment of $56,274 was the total amount he invested. Over the entire 30-year period he never contributed any additional money. Still, the power of compound growth triumphs once again. After 30 years, the value of Ted’s investment portfolio has grown to $799,744! How about that…

Tools To Get You Started

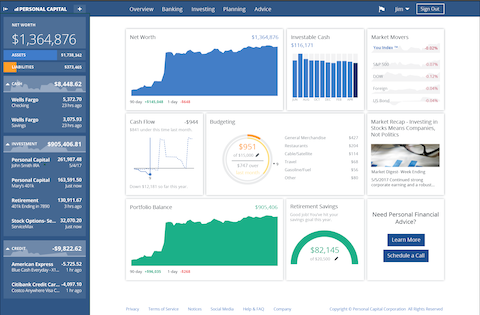

Get a head start on your journey toward achieving financial independence by analyzing and tracking your income, expenses, investment performance, and overall net worth with the free online wealth management tool Empower Personal Dashboard.

We use Empower Personal Dashboard regularly to analyze our investment fees, track our investments, and project our net worth. We also periodically review our progress toward retirement with their retirement planning calculator.

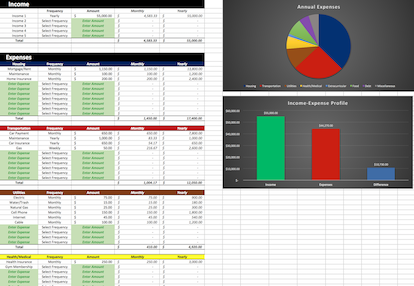

If you’d rather do things on your own, become a subscriber today and you’ll receive our Free Financial Planning Dashboard. This tool allows you to enter your income and expenses to create a detailed budget. You can use it to track your spending habits over time or just to get an idea of where your money is going each month. Take a look at the automatically generated charts and you may discover you have a little more cash to invest than you thought.

If you’re interested in detailed instructions on how to budget, save, pay off debt, and invest, check out The 6 Phases of Building Wealth. This book provides step-by-step instructions for working through each “Phase” in the process of achieving Financial Freedom. If you're just starting out, the information in this book will provide you with an invaluable resource. You can pick up the digital version for only $2.99 on Amazon.

Great article! I think I’m convinced.

In the Bill and Ted part, I initially I missed the part where Ted is investing his extra money each year. That’s a big deal! I went back over it and saw the asterisks though. So the whole thing for that section is basically to make sure you’re investing the leftover cash, I guess!

Absolutely, you’ve got to invest those savings! Also, notice in the second example, even when there where no monthly savings, Ted still came out on top due to the higher return he got from his stock investments.

I completely agree with you on renting and love how detailed your post was. The only thing preventing me from renting and cashing in on our mortgage equity is the volatile rental market. There is such a spike in real estate where we live for the entire region, homes are being bought and sold rapidly creating a volatile rental market. A landlord selling your rental while in a low vacancy market is troubling for many.

Yep. The realities of the housing market you actually live in may determine what the most profitable course of action is. The analysis I did simply show’s averages over time. The specifics of your situation may be completely different. Thanks for the comment!

The rent vs buy discussion has always intrigued me. I like to go into it open-minded and to see it from both viewpoints. Each side makes compelling arguments. It just comes down to personal preference. I see the renting side of things by having a set payment that you know what you can budget for. Then I see buying as a form of owning and it’s yours. I’m more in the middle and would rather have a duplex rental property I own and the renter paying the mortgage. It’s the best of both worlds.

I think the main point is that (for the most part) buying a home to live in is a lifestyle choice and not necessarily a good investment. That doesn’t make it a bad decision. On the contrary, it might be a great decision for you and your family. It’s just not the best use of funds you’d like to invest, on average.

I think that whether you rent a house or buy a house, people are comfortable with the layout of the house and the cleanliness in the house, the money for the house is worth it. I’m in a rented house and I always keep it clean with a cleaning tool like vacuum, mop, … because for me a clean house always brings the highest comfort.